Most parents want the best for their children. For many, that means a college degree. But a quiet crisis is growing in American living rooms. It is called the Parent PLUS loan.

This federal program lets parents borrow for their child’s school. Unlike other student loans, there is no limit on the amount. Parents can borrow the full cost of college. This sounds like a gift, but it often becomes a burden.

According to the College Board, the average cost of a private four-year college is now over $60,000 per year. Many families cannot pay this in cash. They turn to Parent PLUS loans to fill the gap. Now, millions of parents are entering their 50s and 60s with six-figure debt.

The Rapid Growth of Parent Debt

The numbers are startling. A 2024 report from the Peter G. Peterson Foundation found that total student debt has reached $1.75 trillion. A large and growing slice of that belongs to parents. They are not the ones with the degree, but they are the ones with the bill.

Data from the U.S. Department of Education shows that over 3.7 million parents hold these loans. The average balance has climbed steadily over the last decade. Many parents now owe more than $30,000, and many owe much more.

A 2022 study by the Century Foundation highlighted a major problem. They found that low-income families are using these loans more often. These families have the least ability to pay them back. This creates a cycle of debt that lasts for decades.

James Kvaal, the Under Secretary of Education, said in a 2023 statement, “Parent PLUS loans can be a lifeline, but they can also be a weight around the necks of families.” This weight is getting heavier every year.

Why These Loans Are Different

Parent PLUS loans are not like typical student loans. They have higher interest rates. They also have higher fees. According to the Federal Student Aid office, the interest rate for loans issued in mid-2024 was 9.08%.

Private banks often offer lower rates to people with good credit. But the government gives these loans to almost any parent. They do not check if you can afford the monthly payment. They only check for a very poor credit history.

This means a parent making $40,000 a year could borrow $100,000. There is no “ability-to-pay” test. This is why many experts call it a debt trap. The loan grows faster than the parent can pay it off.

A 2023 report from the Brookings Institution found that Parent PLUS borrowers are less likely to see their balances go down. Because of high interest, the total amount owed often goes up over time. This is called negative amortization.

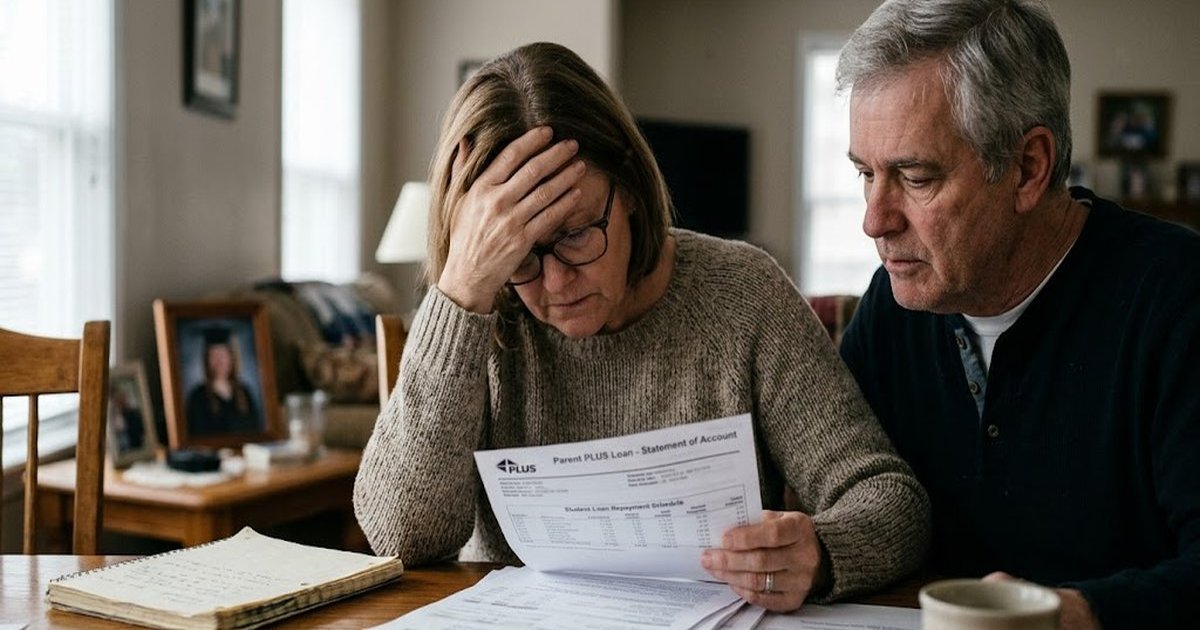

The Impact on Your Retirement

For a 50-year-old woman, retirement is not far away. Every dollar spent on a loan is a dollar not saved for the future. This is where the macro trend hits your personal wallet.

The Social Security Administration warns that many seniors rely on their checks for most of their income. But if you default on a federal loan, the government can take part of your Social Security check. This is known as “offsetting” your benefits.

A 2024 analysis by AARP found that the number of older Americans with student debt has tripled since 2004. Many of these people are parents who borrowed for their kids. They are now facing a choice between paying the government or buying groceries.

Senator Elizabeth Warren has spoken out about this issue. In a 2023 Senate hearing, she said, “We are seeing a generation of seniors who are being pushed into poverty by student loan debt.” This is a reality for thousands of households today.

How to Protect Your Family

You can still help your child without ruining your future. The first step is to set a firm limit. Do not borrow more than you can pay back before you retire. Use a simple loan calculator to see your future monthly bill.

Look at other options first. Students should take out their own federal loans before a parent steps in. Those loans have lower interest rates. They also have more flexible options for repayment based on income.

According to the National Association of Student Financial Aid Administrators, families should also look at “income-driven” plans. However, Parent PLUS loans are only eligible for these plans if you “consolidate” them first. This is a complex step, but it can lower your monthly cost.

Finally, talk to your child. Be honest about what you can afford. A cheaper school might be a better choice for the whole family. A degree is valuable, but your financial safety is also important.

Looking at the Big Picture

The national debt is a major topic in Washington. But for most Americans, their own “national debt” is the one they see on their monthly statement. Parent PLUS loans are a large part of that picture.

The Committee for a Responsible Federal Budget has noted that rising interest rates make this debt even more dangerous. As the government pays more to borrow, families pay more too. Everything is connected in the modern economy.

Education is an investment. But like any investment, it can be too expensive. By understanding the risks of Parent PLUS loans, you can make a smarter choice. You can support your child’s dreams without giving up your own security.

Frequently Asked Questions

What is the current interest rate for a Parent PLUS loan?

For loans issued between July 2024 and July 2025, the interest rate is 9.08%. This is significantly higher than the rates for undergraduate student loans, which are 6.53% for the same period.

Can the government take my Social Security to pay for these loans?

Yes, if you fall behind on payments, the government can take up to 15% of your Social Security benefit. This is a common practice used to recover unpaid federal debt from seniors.

Is there a limit on how much a parent can borrow?

There is no set dollar limit for Parent PLUS loans like there is for student loans. A parent can borrow up to the total “cost of attendance” at the school, minus any other financial aid the student receives.