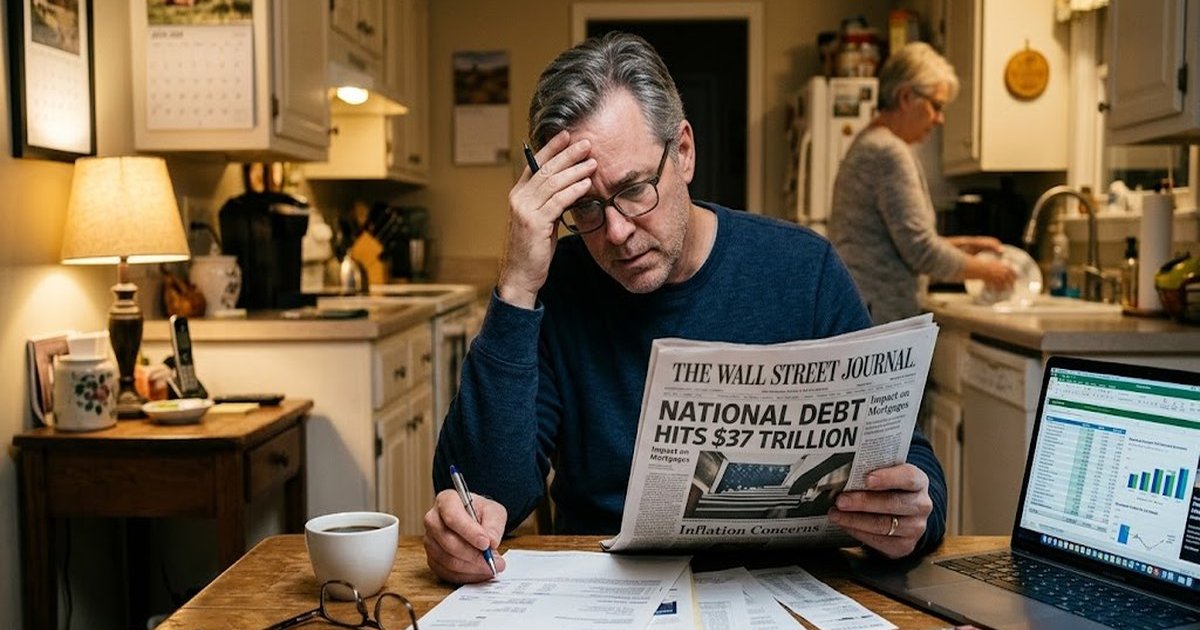

The Massive Size of Our National Debt

The numbers coming out of Washington are truly mind-blowing. According to the U.S. Treasury Department, the national debt has ballooned to roughly $37 trillion. That’s a lot of money.

Seriously, it’s almost impossible to wrap your head around that number. If you were to count one dollar every second, it would take over a million years to reach that amount. Think about that for a moment.

You might be wondering, “Why should I even care? I’ve got my own bills to worry about – groceries, gas, keeping the house warm.”

But here’s the thing: the government’s debt problem isn’t some distant issue. It’s your problem, too. It affects your daily life in sneaky ways, changing the prices you pay and the interest rates you get.

Basically, when the government spends more than it takes in through taxes, it has to borrow the difference. That borrowed money adds up to the national debt.

And over the past few years, the government has been borrowing at a record pace. This borrowing comes with a steep price for everyday Americans.

How Washington’s Borrowing Raises Your Interest Rates

When the government needs cash, it issues Treasury bonds. Investors buy these bonds, essentially lending money to the government. That’s how the borrowing happens.

But there’s only so much money available to be lent out in the world. When the government starts borrowing huge amounts, it sucks up a lot of that available capital.

That leaves less money for banks to lend to regular folks. When money’s tight, banks naturally bump up their interest rates – and that means you pay more to borrow.

Think about it: higher mortgage rates when you’re trying to buy a house. Higher rates on car loans. Even higher fees on your credit cards. Not great, right?

Federal Reserve Chairman Jerome Powell has spoken out about this danger. He noted, “The U.S. federal government is on an unsustainable fiscal path.”

When a path isn’t sustainable, the costs get passed down to you. You end up paying more interest on your personal debts because the government is racking up so much debt.

And if you’re planning on helping your kids pay for college? This matters. Student loan interest rates are also tied to how much the government borrows.

The High Cost of Paying Interest

Just like you have to pay interest on a credit card balance, the government pays interest on its debt. And that interest bill is growing at an alarming rate.

The Congressional Budget Office reports that the government is now spending more on interest payments than it does on national defense! That’s a jaw-dropping figure.

Think about what that means for our country. We’re diverting hundreds of billions of dollars just to service our past debts – money that could be used for the future.

Every dollar spent on interest is a dollar that can’t be used for other critical things. We can’t fix roads, build schools, or keep the country safe. It’s a trade-off.

This creates a huge problem for the federal budget. As the debt grows, the interest payments grow even larger. It’s a vicious cycle, and it’s hard to break free.

Eventually, the government will have to make some tough decisions. To cover this massive interest bill, leaders will have to find more money—and there aren’t a ton of easy options.

What This Means for Social Security and Taxes

To find more money, the government primarily has two options: raise taxes or cut spending on programs people rely on.

If taxes go up, your paycheck will shrink. You’ll have less money to save for retirement or spend on your family. It’s a simple equation.

And if the government cuts spending? Well, many Americans worry that Social Security and Medicare could face cuts down the road.

A 2024 Pew Research Center study found that 57 percent of Americans view the budget deficit as a top priority for the president and Congress. No kidding—people are concerned.

They’re right to be worried. When a huge chunk of the budget goes to interest payments, safety net programs become vulnerable.

For a 50-year-old planning for retirement, this is a real concern. You’ve paid into Social Security your entire working life. You expect it to be there when you stop working.

A massive national debt makes the future of these programs less secure. It forces politicians to look for cuts wherever they can find them.

How the Debt Can Make Inflation Worse

There’s another, rather unpleasant, way the government deals with too much debt: it can just create more money. But this choice comes with a terrible side effect for families.

When the government pumps too much money into the economy, money loses its value. That’s what causes inflation. It makes everything you buy more expensive.

The Bureau of Labor Statistics tracks the prices we pay for everyday goods, reporting them through the Consumer Price Index. They don’t lie.

We all remember what happened when inflation spiked a few years ago. The price of eggs, bread, and milk went through the roof. Your grocery bill grew, but your paycheck didn’t.

High national debt keeps the risk of inflation alive. If the government keeps borrowing and spending, prices will likely stay high, or even rise further.

Inflation is often called a hidden tax. You don’t see it directly on your pay stub, but it quietly steals the buying power of your hard-earned money.

For families trying to stick to a tight budget, inflation is devastating. It forces you to make tough choices about what you can afford at the store.

Smart Ways to Protect Your Family’s Money

You can’t control what politicians do in Washington. You can’t magically stop the national debt from growing.

Here’s the thing: you *can* control your own wallet.

The best way to protect your family is to take a look at your own financial situation. You need to make sure your financial house is in order.

First, focus on paying off any debt that has a variable interest rate. Credit cards are the biggest danger here. When government borrowing pushes rates up, credit card debt gets really expensive.

If you can, try to pay more than the minimum payment. It’s a long game, but it’s worth it.

If you own a home and have a fixed-rate mortgage, you’re in a pretty good spot. Your rate won’t change, even if the government causes interest rates to rise.

Looking Ahead to the Future

$37 trillion is a heavy burden for our country. It will shape our economy for years to come. This isn’t an issue that will simply disappear overnight.

Leaders in Washington will have to face this reality soon. They’ll need to make some tough choices about taxes and spending to fix the problem.

Until they do, you must be the strong leader of your own family’s finances. Stay informed about what’s happening in the economy – and don’t panic.

Make smart choices with your money today. Avoid unnecessary debt and build your savings whenever possible. Be careful, but don’t despair.

By taking these simple steps, you can shield your family from the worst effects of the national debt. You can build a secure future, no matter what happens in Washington.

Frequently Asked Questions

Will the national debt cause a market crash?

No one can perfectly predict the stock market. However, high government debt can slow down economic growth over time. This makes it harder for businesses to grow, which can hurt your retirement accounts.

Does the government ever pay off its debt completely?

The government rarely pays off its total debt balance. Instead, it pays the interest due and borrows new money to pay off old debts. This is much like paying off one credit card with another credit card.

Can the government just print more money to pay the debt?

Yes, the government *can* create more money, but this is a very dangerous move. Printing too much money causes high inflation. This makes your groceries, gas, and everyday needs cost much more.