The Massive Size of Our National Debt

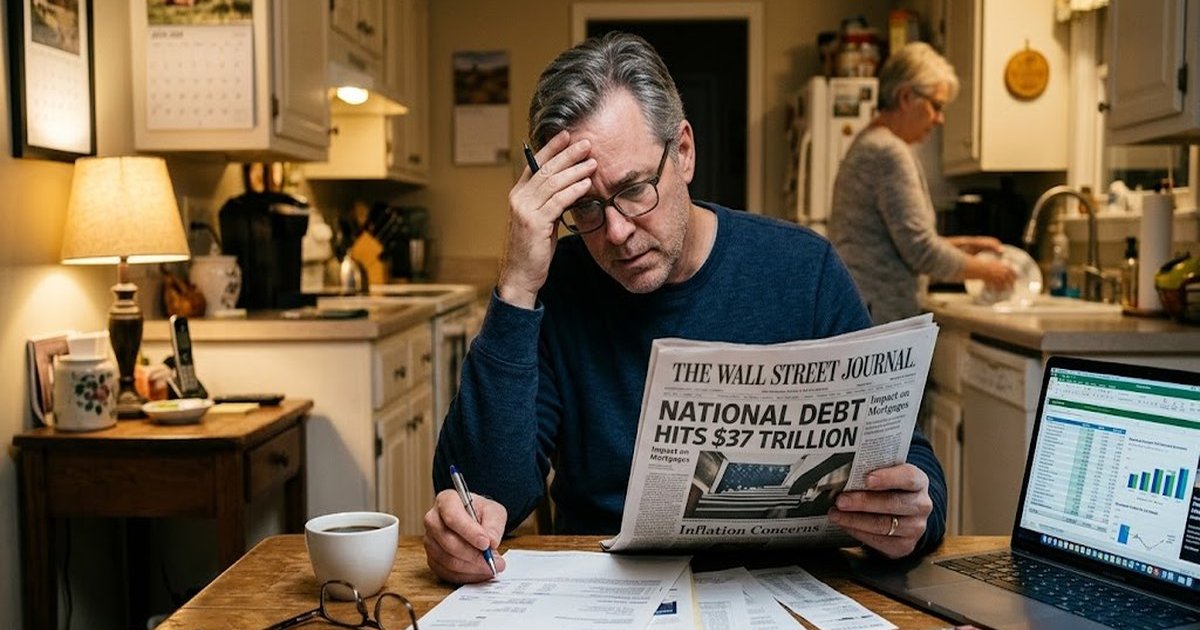

The numbers coming out of Washington are hard to believe. According to the U.S. Treasury Department, the national debt has reached roughly 37 trillion dollars.

This number is so large that it is hard to picture. If you counted one dollar every single second, it would take you over a million years to reach that amount.

You might wonder why you should care about this number. You have your own bills to pay. You worry about the cost of groceries, gas, and keeping your home warm.

But the truth is, the government’s debt problem is your problem, too. It affects your daily life in hidden ways. It changes the prices you pay and the interest rates you get.

When the government spends more money than it takes in from taxes, it must borrow the difference. This borrowed money makes up the national debt.

Over the past few years, the government has borrowed at a record pace. This borrowing comes with a heavy price tag for everyday Americans.

How Washington’s Borrowing Raises Your Interest Rates

When the government needs money, it issues Treasury bonds. Investors buy these bonds, lending their money to the government. This is how the borrowing happens.

But there is a limited amount of money in the world to be lent out. When the government borrows huge amounts, it takes up a lot of that available money.

This leaves less money for banks to lend to normal people. When money is tight, banks raise their interest rates. They charge you more to borrow money.

This means higher mortgage rates when you want to buy a house. It means higher rates for car loans and higher fees on your credit cards.

Federal Reserve Chairman Jerome Powell has spoken about this danger. He said, “The U.S. federal government is on an unsustainable fiscal path.”

When the path is not sustainable, the costs get passed down to you. You end up paying more interest on your personal debts because the government is borrowing so much.

If you plan to help your children pay for college, this matters. Student loan interest rates are also tied to how much the government borrows.

The High Cost of Paying Interest

Just like you have to pay interest on a credit card balance, the government pays interest on its debt. And that interest bill is growing very fast.

The Congressional Budget Office reports that the government now spends more on interest payments than it does on national defense.

Think about what that means for our country. We are spending hundreds of billions of dollars just to service our past debts. That money pays for the past, not the future.

Every dollar the government spends on interest is a dollar it cannot spend on other things. It cannot go toward fixing roads, building schools, or keeping the country safe.

This creates a big problem for the federal budget. As the debt grows, the interest payments grow even larger. It is a vicious cycle that is hard to break.

Eventually, the government will have to make hard choices. To pay this massive interest bill, leaders will have to find more money. There are only a few ways they can do this.

What This Means for Social Security and Taxes

To find more money, the government can do two main things. It can raise taxes, or it can cut spending on programs that people rely on.

If the government raises taxes, your paycheck will shrink. You will have less money to save for your own retirement or spend on your family.

If the government cuts spending, it might target large programs. Many Americans worry that Social Security and Medicare could face cuts in the future.

A 2024 Pew Research Center study found that 57 percent of Americans view the budget deficit as a top priority for the president and Congress.

People are right to be worried. If a large chunk of the budget goes to interest payments, safety net programs become vulnerable.

For a 50-year-old planning for retirement, this is a real concern. You have paid into Social Security your whole life. You expect it to be there when you stop working.

A massive national debt makes the future of these programs less secure. It forces politicians to look for cuts anywhere they can find them.

How the Debt Can Make Inflation Worse

There is another way the government deals with too much debt. It can simply create more money. But this choice comes with a terrible side effect for families.

When the government pumps too much money into the economy, money loses its value. This is what causes inflation. It makes everything you buy more expensive.

The Bureau of Labor Statistics tracks the prices we pay for everyday goods. They report these numbers through the Consumer Price Index.

We all saw what happened when inflation spiked a few years ago. The price of eggs, bread, and milk shot up. Your grocery bill grew, but your paycheck did not.

High national debt keeps the risk of inflation alive. If the government keeps borrowing and spending, prices will likely stay high or rise even further.

Inflation is often called a hidden tax. You do not see it on your pay stub, but it quietly steals the buying power of your hard-earned money.

For families trying to stick to a tight budget, inflation is devastating. It forces you to make tough choices about what you can afford at the store.

Smart Ways to Protect Your Family’s Money

You cannot control what politicians do in Washington. You cannot stop the national debt from growing. But you can control your own wallet.

The best way to protect your family is to look at your own balance sheet. You need to make sure your financial house is in order.

First, focus on paying off any debt that has a changing interest rate. Credit cards are the biggest danger here. When government borrowing pushes rates up, credit card debt gets very expensive.

Try to pay more than the minimum payment each month. If you can clear your credit card balances, you will protect yourself from rising interest rates.

Second, build up your emergency savings. A good rule is to have enough money to cover three to six months of basic living costs.

Keep this emergency money in a safe place. A high-yield savings account is a good option. These accounts actually pay you more interest when national rates are high.

Third, think carefully before taking on new debt. If you need to buy a car, try to save for a larger down payment. This will reduce the amount you have to borrow.

If you own a home and have a fixed-rate mortgage, you are in a good spot. Your rate will not change, even if the government causes interest rates to rise.

Looking Ahead to the Future

The 37 trillion dollar debt is a heavy burden for our country. It will shape our economy for years to come. It is not an issue that will vanish overnight.

Leaders in Washington will have to face this reality soon. They will need to make tough choices about taxes and spending to fix the problem.

Until they do, you must be the strong leader of your own family’s finances. Stay informed about what is happening in the economy.

Do not panic, but do be careful. Make smart choices with your money today. Avoid unnecessary debt and build your savings whenever you can.

By taking these simple steps, you can shield your family from the worst effects of the national debt. You can build a secure future, no matter what happens in Washington.

Frequently Asked Questions

Will the national debt cause a market crash?

No one can perfectly predict the stock market. However, high government debt can slow down economic growth over time. This makes it harder for businesses to grow, which can hurt your retirement accounts.

Does the government ever pay off its debt completely?

The government rarely pays off its total debt balance. Instead, it pays the interest due and borrows new money to pay off old debts. This is much like paying off one credit card with another credit card.

Can the government just print more money to pay the debt?

Yes, the government can create more money, but this is a very dangerous move. Printing too much money causes high inflation. This makes your groceries, gas, and everyday needs cost much more.